Buying the dip is not a singular investment maneuver; it is a bet on mean reversion during periods of temporary liquidity contraction or sentiment-driven selling. For an institutional or sophisticated retail participant, the decision to deploy capital during a market drawdown requires a clinical distinction between transient volatility and structural regime shifts. Most market commentary fails because it treats "the dip" as a uniform event. In reality, a 5% retracement in a secular bull market is a fundamentally different mechanical event than a 5% drop during a period of monetary tightening and earnings compression. To capitalize on these windows, one must quantify the margin of safety and the velocity of the recovery relative to the cost of carry.

The Taxonomy of a Market Drawdown

Successful execution depends on identifying the causal mechanism behind the price action. Market drops generally fall into three distinct categories, each requiring a different strategic response. Don't forget to check out our previous coverage on this related article.

- Liquidity Shocks: These occur when a sudden need for cash—often due to margin calls or exogenous geopolitical shocks—forces institutional selling across uncorrelated asset classes. These are the highest-probability "buy the dip" opportunities because the selling is divorced from the underlying value of the assets.

- Cyclical Adjustments: These are slower, grinding sell-offs driven by changes in the macro environment, such as a shift in central bank policy or a peak in the business cycle. Buying these dips prematurely leads to "catching a falling knife" because the fundamental valuation floor is actively moving lower.

- Structural Breaks: These represent a permanent impairment of value, often seen in specific sectors (e.g., the decline of physical retail) or broader economies facing insolvency. Mean reversion logic fails here because the "mean" itself has shifted downward.

The Calculus of Entry: Risk-Adjusted Timing

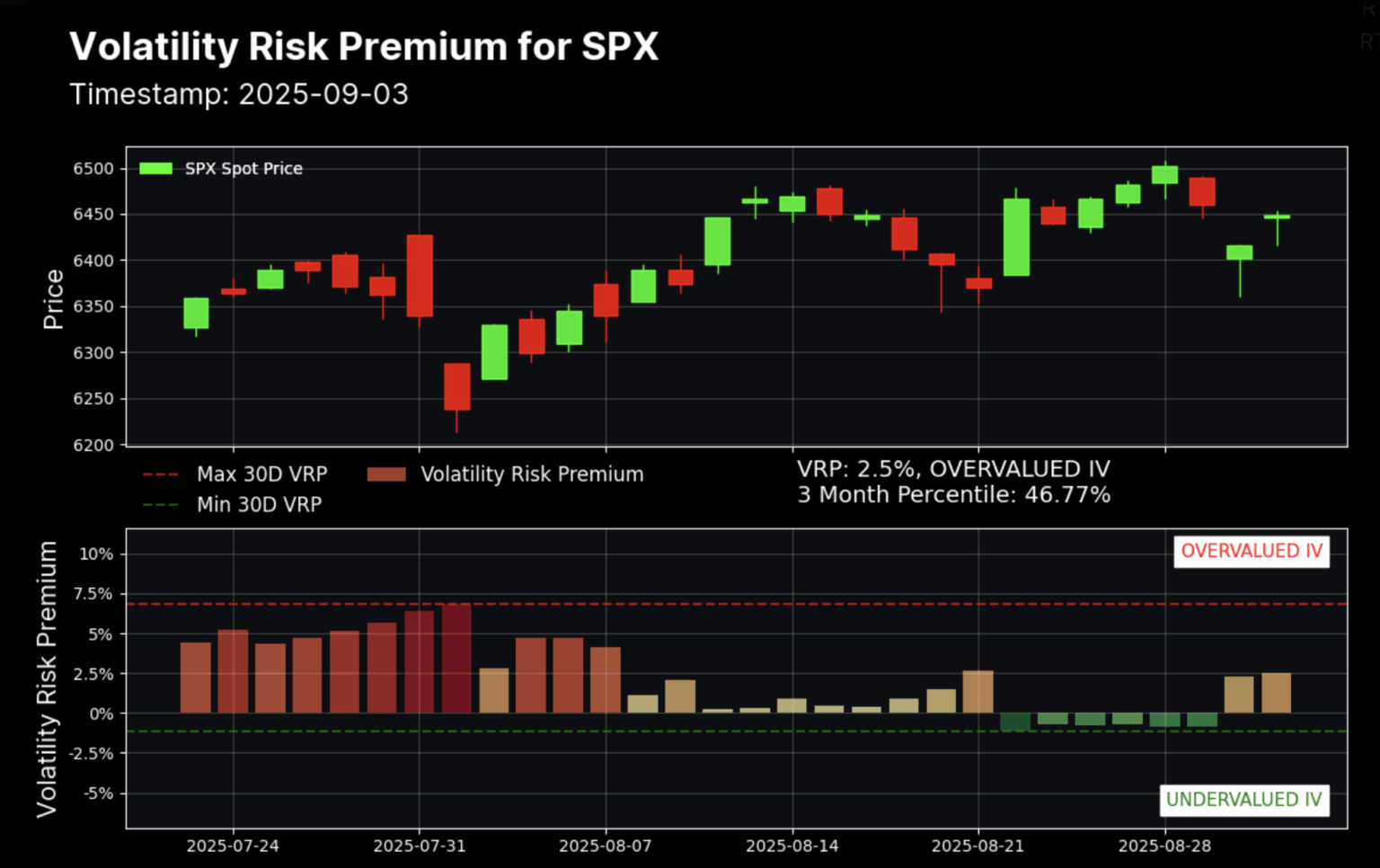

The primary failure in retail "dip buying" is the neglect of the Volatility Risk Premium (VRP). Volatility tends to cluster; a high-volatility day is statistically likely to be followed by another. Entering a position during the initial spike in the VIX (Volatility Index) ignores the fact that the market has not yet reached an equilibrium of "price discovery."

A disciplined strategy utilizes a tiered entry framework based on standard deviations from the 200-day moving average. To read more about the context of this, Business Insider offers an excellent summary.

- The Tactical Entry (1.0 Sigma): A minor retracement often driven by profit-taking. This is suitable for adding to existing winners with high "moat" characteristics.

- The Strategic Rebalancing (2.0 Sigma): A significant correction where emotional selling begins to outweigh rational valuation. This is where the gap between price and intrinsic value begins to widen meaningfully.

- The Capitulation Phase (3.0 Sigma or higher): Extreme outlier events. While these offer the highest historical returns, they also carry the highest risk of "tail risk" events where the system itself faces liquidity constraints.

Calculating the Margin of Safety

To determine if a dip is worth buying, an analyst must run a sensitivity analysis on the Equity Risk Premium (ERP). The ERP represents the excess return that investing in the stock market provides over a risk-free rate, such as a 10-year Treasury bond. When prices drop, the ERP theoretically increases, making stocks more attractive.

However, if the dip is accompanied by rising interest rates, the relative attractiveness of stocks may actually decrease despite the lower price. The formula for the required return ($K_{e}$) can be expressed via the Capital Asset Pricing Model (CAPM):

$$K_{e} = R_{f} + \beta(R_{m} - R_{f})$$

Where $R_{f}$ is the risk-free rate, $\beta$ is the asset's sensitivity to the market, and $(R_{m} - R_{f})$ is the market risk premium. If $R_{f}$ is climbing faster than the price is falling, the "dip" is a statistical illusion of value.

Psychological Arbitrage and the Behavioral Gap

The ability to "buy the dip" is less about financial capital and more about cognitive capital. Retail investors are frequently plagued by "loss aversion," where the pain of a 10% loss is felt twice as intensely as the pleasure of a 10% gain. This creates an opportunity for the disciplined analyst to engage in psychological arbitrage—buying assets from those who are forced to sell by their own emotional thresholds.

Structural bottlenecks often prevent people from buying at the bottom:

- Exhausted Liquidity: Many investors are fully leveraged at the peak and have no dry powder when the dip occurs.

- Narrative Saturation: During a crash, the news cycle generates a feedback loop of negativity that makes a recovery seem impossible.

- Recency Bias: The tendency to believe that because the market fell yesterday, it must fall today.

Overcoming these requires a pre-computed execution plan. One should never decide to buy during the heat of a trading session; the decision must be made when the market is closed, based on predetermined price triggers.

Operational Constraints and Execution Risks

Even a correct thesis can fail due to poor execution. A common mistake is "all-in" deployment. When a market is in a state of high gamma (where price swings accelerate), the probability of an "overshoot" to the downside is high.

The Cost of Premature Deployment

If an investor deploys 100% of their cash at a 10% drawdown, and the market proceeds to a 30% drawdown, the opportunity cost is catastrophic. The investor is now "trapped" in a position with no ability to average down, often leading to a forced exit at the absolute bottom due to psychological exhaustion or margin requirements.

A superior approach is Dynamic Position Sizing. This involves increasing the size of the buy orders as the drawdown deepens. For example:

- At -10% drawdown: Allocate 20% of available cash.

- At -15% drawdown: Allocate an additional 30%.

- At -20% drawdown: Allocate the remaining 50%.

This ensures that the weighted average cost basis is skewed toward the lower end of the curve, maximizing the "coiling" effect of the eventual recovery.

The Secular vs. Cyclical Divide

The most dangerous "dips" are those that occur at the end of a long-term debt cycle. In these instances, the traditional levers of recovery—interest rate cuts and quantitative easing—may have diminished efficacy.

When analyzing a dip, one must check the Credit Impulse. This is the change in new credit issued as a percentage of GDP. If the credit impulse is turning negative, a stock market dip is likely a precursor to a broader economic contraction. In this environment, "buying the dip" is a losing strategy because the corporate earnings ($E$) in the $P/E$ ratio are about to collapse, making the "cheap" stock more expensive on a forward-looking basis.

Portfolio Architecture for Volatility

To effectively buy dips, the portfolio must be architected for resilience before the volatility arrives. This involves maintaining a "barbell" strategy: a core of highly liquid, low-volatility assets (like short-term Treasuries or cash) and a periphery of high-conviction growth assets.

The cash component is not a "dead" asset; it is a perpetual call option on every other asset class with no expiration date and no strike price. The value of this option increases exactly when the market crashes. Without this architectural foundation, "buying the dip" is merely a theoretical exercise rather than a functional strategy.

Strategic Execution Protocol

The transition from analysis to action requires a definitive set of operations. Do not wait for a "clear signal" that the bottom is in; by the time the signal is clear, the most violent part of the recovery has usually passed.

- Identify the Catalyst: If the sell-off is driven by a change in the discount rate (interest rates), adjust valuation models before buying. If it is driven by a "black swan" (unexpected event), prioritize liquidity and quality.

- Audit the Fundamentals: Verify that the long-term earnings power of the target companies remains intact. A dip caused by a product failure is a "trap"; a dip caused by a macro-panic is an "opportunity."

- Execute via Limit Orders: Avoid market orders during high volatility. Wide bid-ask spreads can erode the margin of safety instantly. Set staggered limit orders at key technical support levels and "walk away."

- Monitor the VIX Term Structure: When the front-month VIX futures are priced significantly higher than the back-month (backwardation), it signals extreme short-term panic. This is often the optimal window for deployment, as it indicates the market is paying a massive premium for immediate protection.

Stop looking for "expert" consensus. Experts are incentivized to be cautious during crashes to protect their reputations. The highest returns are found in the delta between the objective reality of corporate cash flows and the temporary insanity of a panicked market. Deploy capital when the cost of the Volatility Risk Premium exceeds the logical risk of the underlying business.