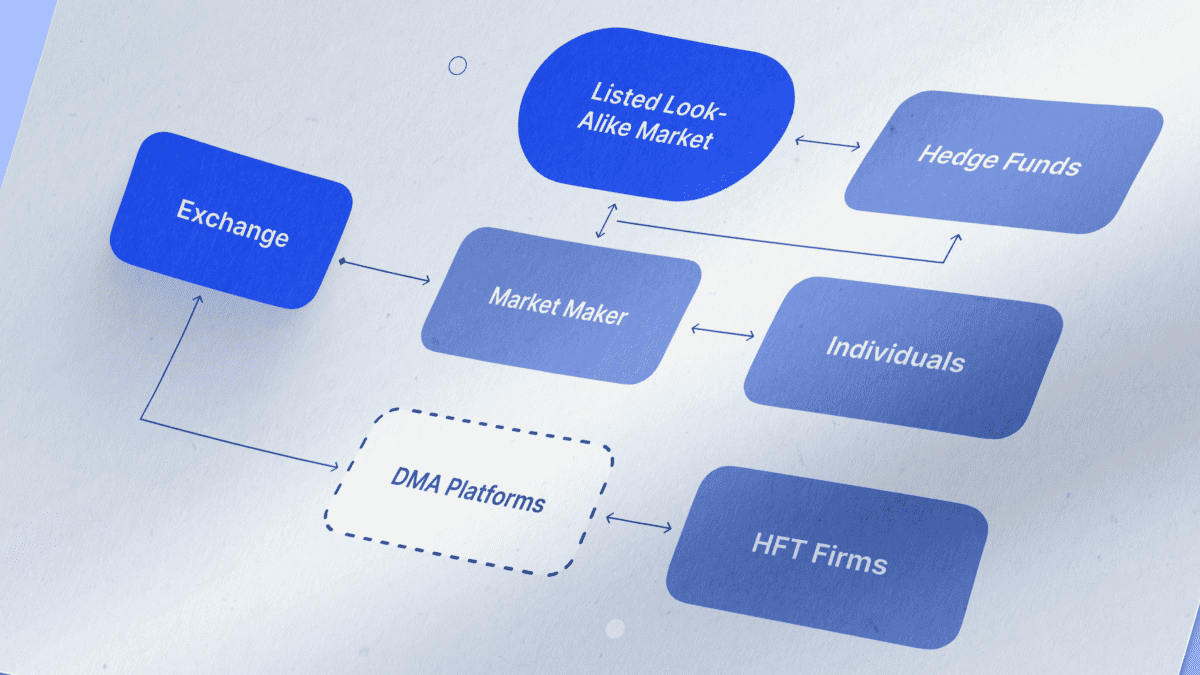

The viability of a prediction market depends entirely on its ability to price tail-end risks that traditional financial instruments ignore or misinterpret. While Kalshi co-founder Luana Lopes Lara often frames the company’s trajectory through the lens of personal risk-taking, the structural reality of the industry is defined by a trilemma of liquidity, regulatory compliance, and information asymmetry. To understand why a prediction market succeeds where a traditional sportsbook or a futures exchange fails, one must quantify the specific frictions inherent in trading "event contracts."

Prediction markets operate as decentralized or centralized truth-engines. Their primary utility is not gambling, but the aggregation of disparate data points into a single, tradable probability. The risk profile of building such an exchange is not merely a matter of "betting on oneself"; it is an exercise in managing the cost of capital against the shifting "No-Action Letters" of federal regulators. Read more on a similar issue: this related article.

The Trinitarian Risk Model of Event Contracts

Every event contract listed on an exchange like Kalshi or Polymarket is subject to three distinct vectors of failure. If any one of these vectors is mismanaged, the market collapses into a zero-liquidity environment or a legal liability.

- Oracular Failure: The risk that the "source of truth" used to settle a contract is ambiguous, corrupted, or disappears. If a contract depends on a specific NASA report that is delayed due to a government shutdown, the capital is locked, the opportunity cost rises, and the platform’s credibility erodes.

- Adverse Selection: The "Informed Trader" problem. Unlike a stock market where insider trading is a regulated crime, prediction markets often rely on people with superior information to move the price toward the truth. However, if the information gap between the "insider" and the "retail liquidity provider" is too wide, the retail side stops participating, and the market dies.

- Jurisdictional Fragility: The Commodity Futures Trading Commission (CFTC) views event contracts through the lens of the Commodity Exchange Act. The risk here is binary: either the contract is deemed "contrary to the public interest" (such as political elections or "gaming") or it is accepted as a legitimate hedging tool.

The Liquidity Trap in Emerging Markets

A common misconception in the growth of prediction markets is that "more events equal more users." In reality, spreading liquidity across too many niche contracts—such as the exact date of a celebrity breakup or specific weather patterns in unpopulated regions—creates a "thin market" problem. Further analysis by CNET explores related perspectives on the subject.

In a thin market, the bid-ask spread is wide. For an institutional hedger looking to use Kalshi to offset the risk of a port strike, a wide spread represents a direct tax on their insurance. The "risk" taken by the founders was not the choice to start a company, but the choice to pursue a Designated Contract Market (DCM) license. This path requires a massive upfront capital expenditure and a multi-year lead time compared to offshore, crypto-native competitors who bypass the CFTC entirely.

The cost of this regulatory compliance is a massive drag on the "speed-to-market" for new contract types. While an offshore platform can spin up a market on a viral news story in minutes, a regulated US exchange must ensure every contract meets the "economic purpose" test. This creates a bottleneck where the exchange is always three steps behind the cultural zeitgeist, trading immediate relevance for long-term institutional trust.

The Calculus of the "Public Interest" Standard

The most significant hurdle for prediction markets in the United States is the subjective nature of Section 5c(c)(5)(C) of the Commodity Exchange Act. This allows the CFTC to ban any contract it deems involves "activities that are unlawful under any Federal or State law; or ... relate to ... gaming."

The strategic pivot for Kalshi was moving beyond simple "betting" to "hedging." To outclass the competition, the logic must shift from "will X happen?" to "how much will it cost me if X happens?"

- Mortgage Rates: A homebuyer uses a prediction market to hedge against a 50-basis-point hike before their closing date.

- Student Loan Forgiveness: A borrower hedges against the Supreme Court striking down a debt-relief plan.

- Recession Probabilities: A small business owner buys "Yes" contracts on a recession to offset potential revenue losses.

By framing these as insurance-like products, the exchange mitigates the "gaming" label. However, this creates a new risk: the basis risk. This is the gap between the payout of the prediction market contract and the actual loss suffered by the hedger. If the correlation between the market outcome and the real-world financial impact is weak, the product loses its economic utility.

Engineering the Truth via Incentive Alignment

The resilience of a prediction market depends on its settlement mechanism. In the case of Kalshi, the reliance on a centralized, regulated clearinghouse provides a "legal finality" that decentralized platforms lack. However, the trade-off is the loss of the "wisdom of the crowd" in the adjudication phase.

In a decentralized model (like Augur or Polymarket), if the outcome of an event is disputed, a token-weighted vote usually decides the winner. This introduces Governance Risk: the possibility that a majority of token holders will vote for a lie if it benefits their financial position.

Kalshi’s model eliminates governance risk but replaces it with Operational Concentration Risk. The exchange becomes the sole arbiter. The "biggest risk" Lara and her team face is not a bad trade by a user, but a single "incorrect" settlement that triggers a class-action lawsuit or a CFTC audit. One faulty data feed on a high-volume contract could bankrupt the clearinghouse.

The Competitive Moat of "Regulated-Only" Capital

There is a distinct segment of capital—pension funds, family offices, and corporate treasuries—that cannot touch unregulated or crypto-based platforms. This is the "Whale Liquidity" that prediction markets need to reach maturity.

The strategy of seeking a DCM license was an intentional play for this specific capital pool. While it limited growth in the 2020-2023 window, it positioned the company as the only viable exit for institutions looking to trade macro-volatility without violating their compliance charters.

The "Risk" here was a bet on the persistence of the American regulatory hegemony. If the world shifted toward decentralized finance faster than expected, the DCM license would become an expensive paperweight. Instead, the slow collapse of offshore, unregulated entities (like FTX) validated the "slow and steady" regulatory approach.

Structural Incentives and Market Manipulation

Any market with low volume is susceptible to "painting the tape"—where a single actor places trades to create a false impression of probability. In prediction markets, this is often used for "perception hacking." A political campaign might buy up "Yes" contracts for their candidate to influence media narratives.

To combat this, a sophisticated exchange must implement:

- Position Limits: Capping the maximum amount a single entity can hold in one contract.

- Identity Verification (KYC): Ensuring that "the crowd" isn't actually one person with a thousand accounts.

- Dynamic Fee Structures: Increasing the cost of trades that move the price significantly beyond historical volatility.

These measures, while necessary for market integrity, actively discourage the "Degenerate" traders who provide the bulk of the volume on unregulated sites. This leads to the Niche Market Paradox: the more "fair" and "regulated" you make the market, the less "exciting" it is for the speculative retail base that usually jumpstarts liquidity.

The Probability of Regulatory Capture

The endgame for prediction markets is not just to coexist with traditional finance, but to replace or augment the "Expert Class." If a market consistently predicts the Fed’s moves better than the Fed’s own economists, the market becomes the authority.

This creates a tension with the state. If the "market" predicts a 90% chance of a government-led project failing, it creates a self-fulfilling prophecy where private contractors pull out, ensuring the project fails. This feedback loop is the ultimate risk. Regulators may eventually view prediction markets not as "gaming" or "hedging," but as a threat to administrative control.

The tactical move for an exchange in this position is to integrate directly with existing financial infrastructure. Rather than standing alone, the data from prediction markets must be fed into Bloomberg Terminals and Reuters Eikon as a standard "Risk Metric." Once the data is indispensable to the 1%, it becomes "too big to ban."

Identify the specific "Economic Purpose" of your most successful contracts and strip away any marketing language that mirrors sports betting. The survival of the event-contract asset class depends on its transition from a "prediction market" to a "contingent-claim insurance layer." If your liquidity providers are primarily speculators rather than hedgers, your platform is a casino in a suit. To scale, you must prioritize contracts where the "No" side is held by those who stand to lose if the event occurs, and the "Yes" side is held by those providing the "insurance" capital. This creates a sustainable, two-sided market that withstands both regulatory scrutiny and market volatility.