You’ve likely seen the headlines about the 2.8% cost-of-living adjustment (COLA) for 2026. On paper, it looks like a win. The average retiree is seeing about $56 more in their monthly check. But if you think that money is yours to keep, I have some bad news. Between rising Medicare premiums and stagnant federal tax brackets, a large chunk of that "raise" is already spoken for.

Most people don’t realize that the thresholds for taxing Social Security haven't changed since the 1980s. While your benefits go up with inflation, the income levels that trigger a tax bill do not. This creates a phenomenon called "bracket creep" for seniors. In 2026, more retirees than ever will find themselves handing their COLA increase right back to the IRS.

The COLA Give and Take

The 2.8% bump for 2026 isn't just a number; it’s a double-edged sword. If you’re a retired worker, your average benefit jumped from $2,015 to $2,071. That seems great until you look at the new Medicare Part B premiums. The standard monthly premium is climbing to $202.90. That’s a nearly 10% hike from last year.

Since most people have their Medicare premiums deducted directly from their Social Security checks, that $17.90 increase immediately eats about a third of your average COLA. If you’re also hit with a higher tax bill because your total income now crosses a decades-old threshold, you might actually end up with less "real" money than you had in 2025.

Why Your 2026 Tax Bill Might Surprise You

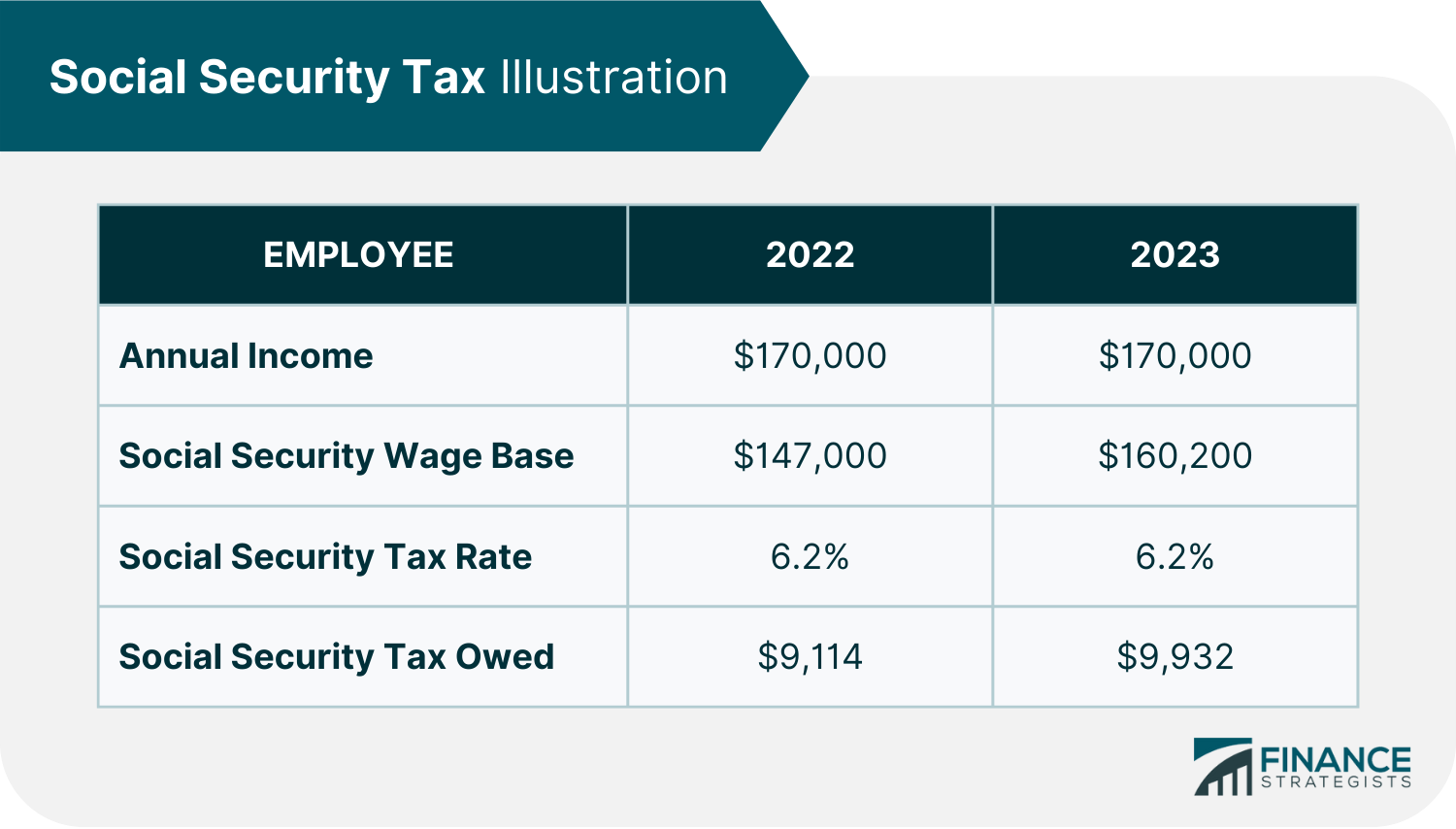

Federal law dictates that if your "combined income" exceeds a certain amount, you owe taxes on up to 85% of your benefits. The formula for combined income is your Adjusted Gross Income (AGI) plus nontaxable interest plus 50% of your Social Security benefits.

Here is the problem: those thresholds are stuck in the past.

- Individuals: If your combined income is between $25,000 and $34,000, you pay tax on 50% of your benefits. Above $34,000, it’s 85%.

- Couples: Between $32,000 and $44,000, you pay tax on 50%. Above $44,000, it’s 85%.

Because these numbers aren't adjusted for inflation, every time you get a COLA increase, you get closer to—or further into—these tax brackets. In 2026, millions of seniors who were previously "tax-free" will suddenly owe the IRS because their 2.8% raise pushed them over the $25,000 or $32,000 line. It’s a stealth tax that targets the middle class, and honestly, it’s a mess.

New Legislation That Actually Helps

There is a bit of a silver lining thanks to the "One Big Beautiful Bill" (OBBB) passed recently. While it didn't fix the federal tax thresholds mentioned above, it did introduce a brand-new senior bonus deduction.

For the 2026 tax year, eligible seniors age 65 and older can claim an additional deduction of up to **$6,000** ($12,000 for married couples). This is huge. It effectively raises the amount of income you can earn before you start paying federal income tax. The full deduction applies if you’re a single filer making under $75,000 or a joint filer under $150,000. It’s temporary, scheduled to vanish after 2028, so you need to take advantage of it while it’s here.

The Status of the You Earned It You Keep It Act

You might have heard rumblings about a bill called the You Earned It, You Keep It Act. This legislation aims to eliminate federal taxes on Social Security benefits entirely. To pay for it, the bill proposes raising the cap on the Social Security payroll tax for high earners—specifically those making over $250,000.

As of early 2026, this bill is still sitting in Congress. If it passes, it would be a total game-changer for the average retiree. But for now, don't count on it. Plan your 2026 budget based on the rules we have today, not the ones we wish we had.

State Taxes Are Moving in a Better Direction

While the federal government is slow to move, states are actually stepping up. In 2026, West Virginia officially completes its phase-out of Social Security taxes. That means all benefits will be fully exempt on your state returns.

Currently, only nine states still tax Social Security to some degree:

- Colorado

- Connecticut

- Minnesota

- Montana

- New Mexico

- Rhode Island

- Utah

- Vermont

- Virginia (though mostly exempt for many)

Even in these states, the rules are changing. For example, Minnesota and New Mexico have significantly raised their income limits for exemptions lately. If you live in one of these areas, check your local tax code—you might be eligible for a break you didn't have two years ago.

The Retroactive Payment Headache

If you were one of the 2.8 million people helped by the Social Security Fairness Act (which repealed the Windfall Elimination Provision and Government Pension Offset), you probably received a fat lump-sum check in 2025.

Here’s the catch: that back pay is treated as income in the year you received it. If you got $15,000 in retroactive benefits last year, that's going on your 2025 tax return (the one you're filing right now in early 2026). This could easily spike your income enough to trigger higher Medicare premiums (IRMAA) or push you into a higher tax bracket.

There is a bipartisan effort called the No Tax on Restored Benefits Act trying to fix this by excluding those specific payments from taxable income. It’s a "wait and see" situation, but keep an eye on it if you received a settlement.

How to Protect Your Benefits in 2026

You aren't totally helpless against these changes. Since the tax is based on "combined income," the goal is to keep that number as low as possible without hurting your lifestyle.

- Use Qualified Charitable Distributions (QCDs): If you’re over 70½, you can send up to $105,000 (the 2026 inflation-adjusted limit) directly from your IRA to a charity. This counts toward your Required Minimum Distribution (RMD) but doesn't count as income on your tax return.

- Watch Your Capital Gains: Selling a winning stock to fund a vacation might seem like a good idea, but the capital gain adds to your AGI. That could be the "final straw" that makes your Social Security taxable.

- Roth Conversions: If you haven't started Social Security yet, consider converting some of your Traditional IRA to a Roth IRA now. Roth withdrawals don't count toward the "combined income" formula later.

Don't wait until next April to figure this out. Grab your 1099-SSA when it arrives, look at your total income sources, and run a quick projection. If you're hovering right near that $25,000 or $32,000 mark, even a small adjustment to your withdrawals could save you thousands in taxes.

Check your "my Social Security" account online right now to see your exact 2026 benefit amount. Once you have that number, compare it against the 2026 standard deduction—which is $17,750 for single seniors—to see where you stand.