The air in a high-stakes private equity suite doesn't smell like gunpowder. It smells like expensive espresso, pressurized oxygen, and the faint, ozone tang of high-end server racks. Here, thousands of miles from the jagged terrain of the Middle East, war is not a tragedy of shrapnel and displacement. It is a "distraction."

Marc Nachmann, a top-tier executive at Goldman Sachs, recently articulated a sentiment that has been rippling through the corridors of global finance. He noted that many private market clients were actually "glad" for the geopolitical tension currently boiling over between Israel and Iran.

To a person watching the evening news with their head in their hands, this sounds like gallows humor at best and sociopathy at worst. But in the world of private markets—where trillions of dollars are locked away in long-term bets—the "distraction" serves a very specific, clinical function. It provides a narrative bridge over a very deep, very scary canyon.

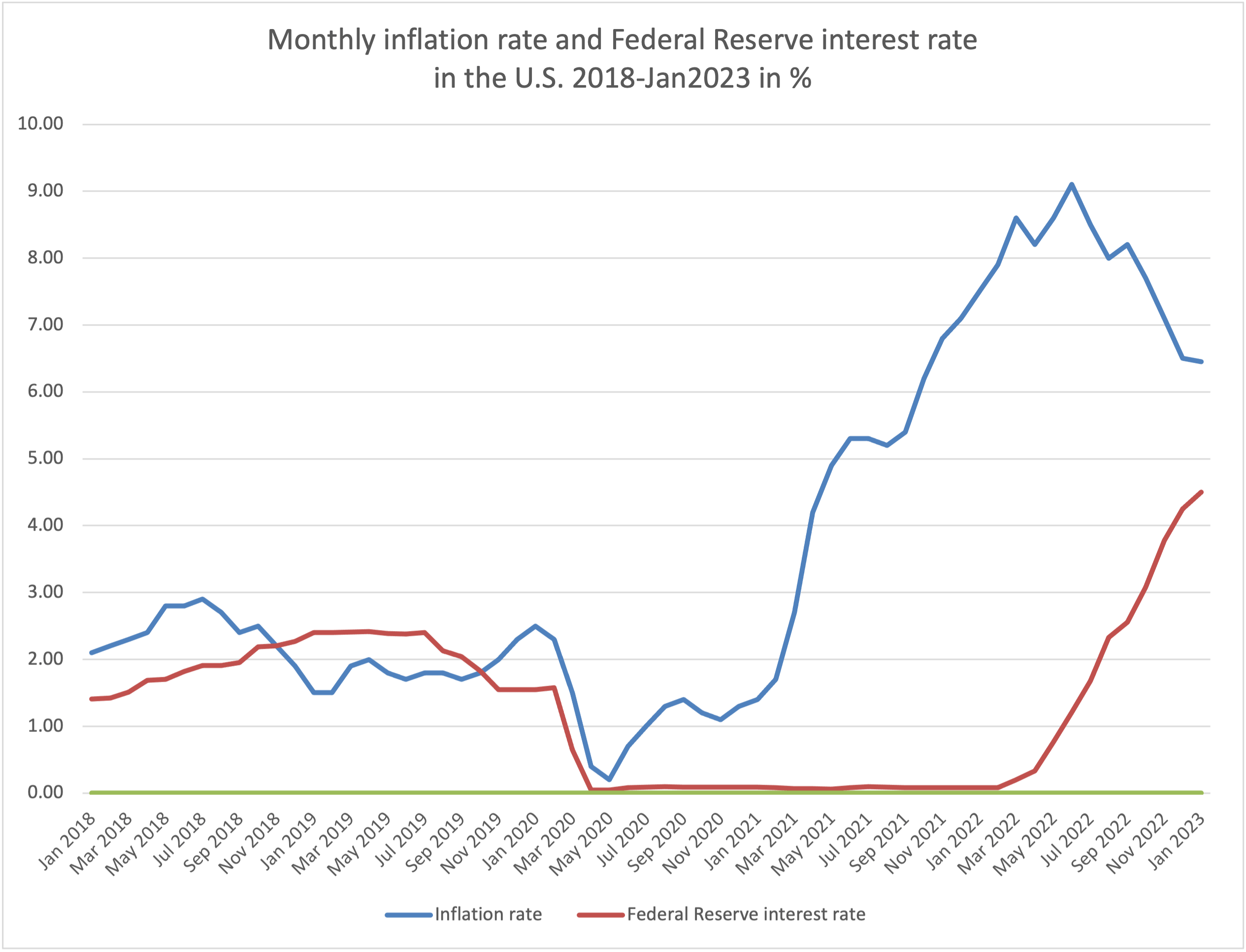

Consider a hypothetical fund manager we will call Elias. Elias sits in a glass-walled office in Midtown Manhattan, staring at a screen that tells him his portfolio of mid-sized software companies is losing its luster. For two years, the conversation in every board meeting has been the same. High interest rates. Stubborn inflation. The Federal Reserve's next move. Every investor who calls Elias asks the same question: "When will the rates drop so my money starts moving again?"

This is the pressure cooker of the private equity world. It is a world where "higher for longer" interest rates act like a slow-moving hydraulic press, squeezing the margins of companies that were bought with cheap debt in 2020. Elias doesn't have an answer for the Fed. No one does.

But then, the geopolitical "distraction" arrives.

Suddenly, the conversation shifts. The headlines on the Bloomberg Terminal are no longer about the 10-year Treasury yield or the Consumer Price Index. They are about troop movements, drone strikes, and the stability of the Strait of Hormuz. For a brief, cold moment, the investor on the other end of the line stops asking about the Fed. They ask about the war. They ask about stability. They ask about the price of oil.

In the language of Goldman Sachs, this is a relief. Not because war is good—everyone in that room would tell you they prefer peace—but because war is a variable they can understand. It is a "known unknown." It moves the focus away from the grinding, mathematical failure of the domestic economy and onto the grand, cinematic stage of international conflict.

The math of $10 trillion in private assets is a heavy thing to carry. Since the 2008 financial crisis, the private equity industry has swelled to gargantuan proportions. It has moved from the fringes of finance to the very center of how the world’s wealth is managed. Pensions, university endowments, and sovereign wealth funds are all heavily "illiquid." This means the money is tied up. You can't just sell your stake in a suburban hospital chain or a logistics company the way you can sell a share of Apple.

When interest rates were near zero, this was a gold mine. You borrowed money for nothing, bought a company, and watched its value rise. But now, the debt is expensive. The exits—selling the company to someone else or taking it public—have frozen over.

Imagine trying to steer a massive cargo ship through a narrow canal while the tide is going out. You are scraping the bottom. You are stuck. Then, a massive storm blows in from the sea. It doesn’t solve your problem of being stuck in the mud, but it gives everyone on the shore a different reason to look away. It gives you a story to tell.

This "distraction" is essentially a psychological pressure valve. For the clients Goldman Sachs serves, the geopolitical tension provides a justification for the stagnation of their portfolios. It’s easier to tell a board of directors that a regional war is causing market volatility than it is to admit that the entire business model of the last decade was predicated on a zero-interest-rate world that may never return.

Nachmann’s observation reflects a chillingly pragmatic truth about how the world’s most powerful people process catastrophe. To them, a war is a data point. It is a volatility spike. It is a reason to hold onto cash or a reason to pivot into defense stocks.

But the human element remains, even if it is invisible in the spreadsheets. Behind every "distraction" are real-world consequences that eventually find their way back to the quiet rooms of Manhattan. A spike in oil prices due to Middle Eastern instability doesn't just change a "input cost" cell in an Excel sheet. It changes the price of milk in a grocery store in Ohio. It changes the heating bill for a family in London.

Eventually, the distraction fades. The smoke clears, and the fundamental reality of the economy remains. The "higher for longer" interest rates are still there. The debt is still expensive. The cargo ship is still stuck in the canal, and the tide is still going out.

The private markets are currently holding their breath. They are grateful for the momentary shift in focus because it buys them time—time to restructure, time to wait for a miracle, time to hope the Fed blinks.

But hope is not a strategy. And a distraction is not a solution.

As the sun sets over the Manhattan skyline, lighting up the glass towers where the world's wealth is managed, the reality remains unchanged. The trillion-dollar bets are still on the table. The clock is still ticking. And the only thing more dangerous than a war is the belief that it can save you from your own math.

The world moves on. The headlines change. The espresso machine in the Goldman suite hisses, ready for the next shift. The executives look at their screens, waiting for the next signal, the next pivot, the next reason to tell their clients that everything is under control, even when the ground beneath them is shifting like sand.

Peace is a quiet thing. It requires a clear-eyed look at the truth. But in the high-stakes game of global finance, truth is often the most expensive commodity of all.

The ledger must always be balanced, whether by the stroke of a pen or the roar of an engine.