The financial press is currently obsessed with a fairytale. They want you to believe that the Federal Reserve and the Bank of England are "diverging" because of unique domestic pressures or differing views on the war in Ukraine. This narrative is comfortable. It suggests that central bankers are independent maestros playing different tunes on the same stage.

It is also complete nonsense.

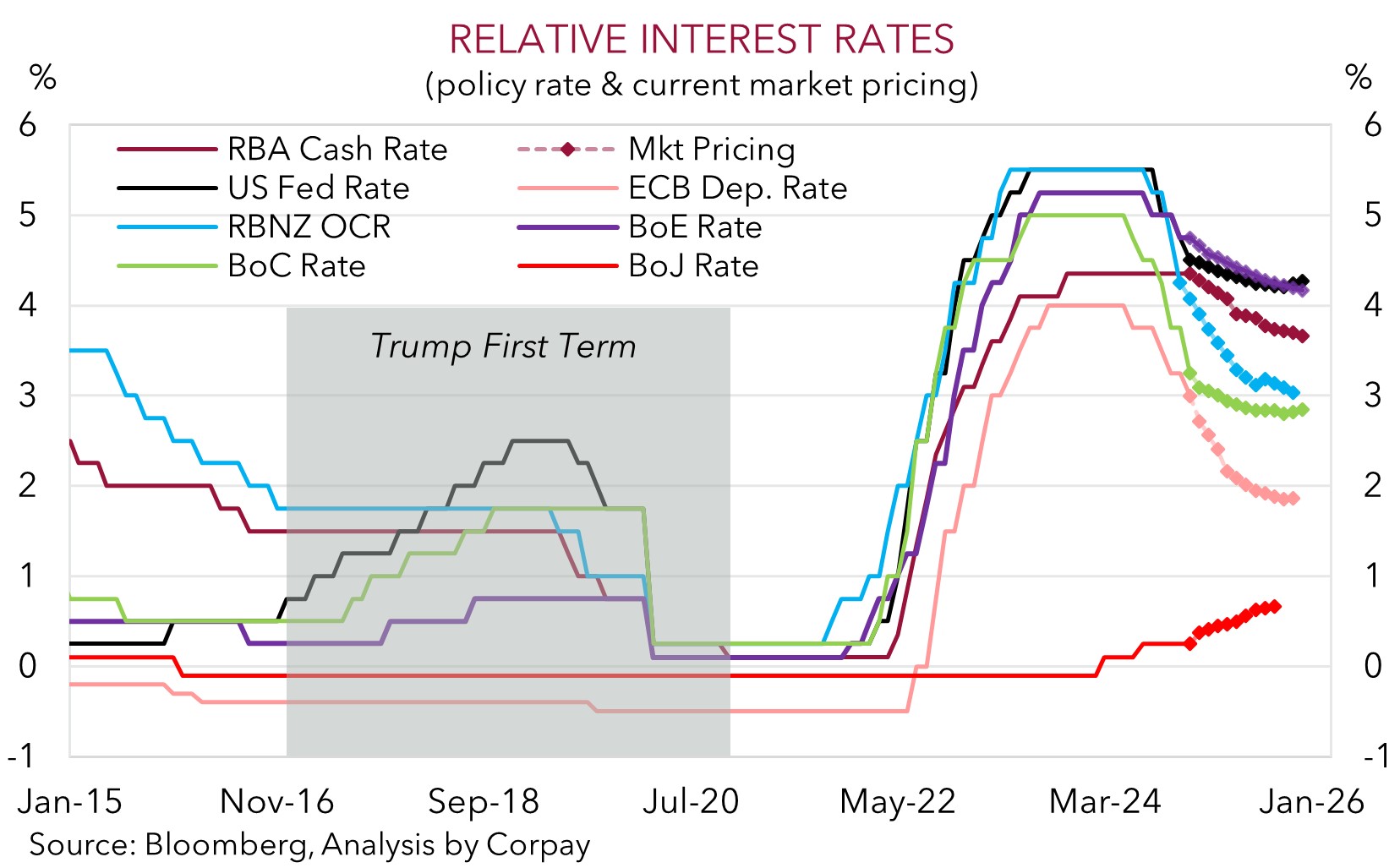

The idea that Jerome Powell and Andrew Bailey are operating from different playbooks because of geopolitical "nuance" ignores the cold reality of the global dollar system. There is no divergence; there is only a delay. The Bank of England isn't choosing a different path—it is simply trapped in a different room of the same burning building.

The Geography of Inflation is a Distraction

Mainstream analysts argue that the Fed is aggressive because the U.S. is insulated from the energy shock, while the BoE is cautious because the UK is a net energy importer feeling the direct blast of the war. This is a surface-level observation masquerading as deep insight.

Inflation isn't a localized weather pattern. It is a monetary phenomenon exacerbated by supply chain fragility. The Fed isn't hiking faster because it "understands" the war better. It is hiking because it owns the world’s reserve currency and must protect the dollar's purchasing power at all costs to prevent a global collapse of faith in U.S. debt.

The Bank of England, meanwhile, is paralyzed. If they hike too fast, they crush a housing market built on a deck of cards. If they hike too slow, the Pound sterling gets slaughtered against the Greenback, importing even more inflation. Calling this "divergence" is like saying a drowning man and a man in a rainstorm have different "philosophies on water."

The Myth of the Independent Central Bank

We need to stop pretending these institutions are independent of the fiscal nightmares their governments created. The "divergence" narrative serves as a convenient smokescreen for the fact that both banks are essentially monetizing debt.

In the U.S., the Fed is trying to cool a labor market that is supposedly "too hot." In the UK, the BoE is dealing with a workforce that has essentially shrunk due to structural failures. The result is the same: higher costs. The competitor article likely suggests that the Fed is "leading" while the BoE is "reacting."

The truth? They are both lagging behind a reality they failed to predict in 2021. I have spent years watching traders lose shirts because they believed the "forward guidance" of these institutions. Forward guidance is not a promise; it is a prayer. When the Fed moves, the rest of the world eventually follows or dies. There is no third option.

Why the "Energy Exposure" Argument is Flawed

Let’s look at the mechanics. The argument goes: "The U.S. is an energy exporter, so they can afford higher rates. The UK is an importer, so they can't."

This ignores the Global Value Chain.

- U.S. companies rely on European components.

- European manufacturers rely on Asian raw materials.

- Everything is priced in Dollars.

When the Fed raises rates, it exports inflation to everyone else. The BoE isn't "diverging" because of the war; it is desperately trying to manage the exchange rate volatility caused by the Fed's dominance. If the BoE doesn't keep pace, the GBP/USD pair drops, making every barrel of oil and every therm of gas—which are priced in dollars—more expensive for the British consumer.

The Thought Experiment: The Island of Solvency

Imagine a scenario where the UK suddenly discovered it was energy independent tomorrow. Would the BoE diverge then? No. They would still be beholden to the global interest rate environment set by the FOMC. If the world’s risk-free rate (the U.S. 10-year Treasury) hits $5%$, capital will flee the UK for the U.S. unless the BoE offers a competitive yield.

The "war" is a convenient scapegoat for structural incompetence. It allows central bankers to say, "We would have fixed this, but then Putin moved." It’s a lie. Inflation was already at $5%$ and $6%$ before the first tank crossed the border. The divergence is a temporary lag in the inevitable march toward higher-for-longer rates across the board.

The Real Divergence is in Social Tolerance

If you want to find the real difference between London and Washington, don't look at the spreadsheets. Look at the streets.

The U.S. has a higher tolerance for economic volatility. Americans are used to a "hire and fire" culture and a more dynamic, albeit brutal, labor market. The UK is gripped by a fear of "stagflation" that is as much psychological as it is economic. The BoE is terrified of being the entity that finally breaks the British middle class.

But here is the hard truth: the market doesn't care about your social contract.

Stop Asking if They Are Diverging

You are asking the wrong question. You should be asking: "How long can the BoE pretend it has a choice?"

The answer is: until the currency market breaks them. We saw a glimpse of this during the LDI (Liability Driven Investment) crisis. The moment the market loses faith in the "divergence" and realizes the UK cannot afford its own debt, the BoE is forced to intervene.

They aren't diverging; they are in a Mexican standoff with reality.

Actionable Intelligence for the Skeptic

- Ignore the Headlines: When you see "BoE holds rates while Fed hikes," don't read it as a policy shift. Read it as a credit risk warning for the UK.

- Watch the Spreads: The only metric that matters is the yield spread between Gilts and Treasuries. If that widens too far, the Pound collapses.

- Bet on Correlation: In a crisis, all correlations go to 1. The idea that you can diversify your portfolio by betting on "divergent" central bank policies is a recipe for a margin call.

The war in Ukraine changed the speed of the decline, but it didn't change the direction. The U.S. and the UK are on the same path toward a massive deleveraging event. One is just walking slightly faster than the other.

The Fed is the engine. The BoE is the caboose. Anyone telling you the caboose is "choosing" a different track hasn't looked at the rails.

Stop looking for nuance where there is only gravity.