Jim Cramer calls Babcock & Wilcox a "great spec." That phrase alone should make your skin crawl. In the world of institutional capital, "spec" is often just polite shorthand for a company that has burned through its balance sheet and is now praying for a regulatory miracle. If you are buying BW because a television personality gave it a ten-second nod between sound effects, you aren't investing. You are subsidizing a legacy industrial firm’s attempt to hallucinate a green future.

The "lazy consensus" here is seductive. The narrative claims that a century-old boiler company can pivot into carbon capture, hydrogen, and renewable energy, capturing the massive tailwinds of the global energy transition. It sounds logical on paper. In reality, it ignores the brutal physics of industrial scaling and the even more brutal math of their debt profile.

The Thermal Paradox

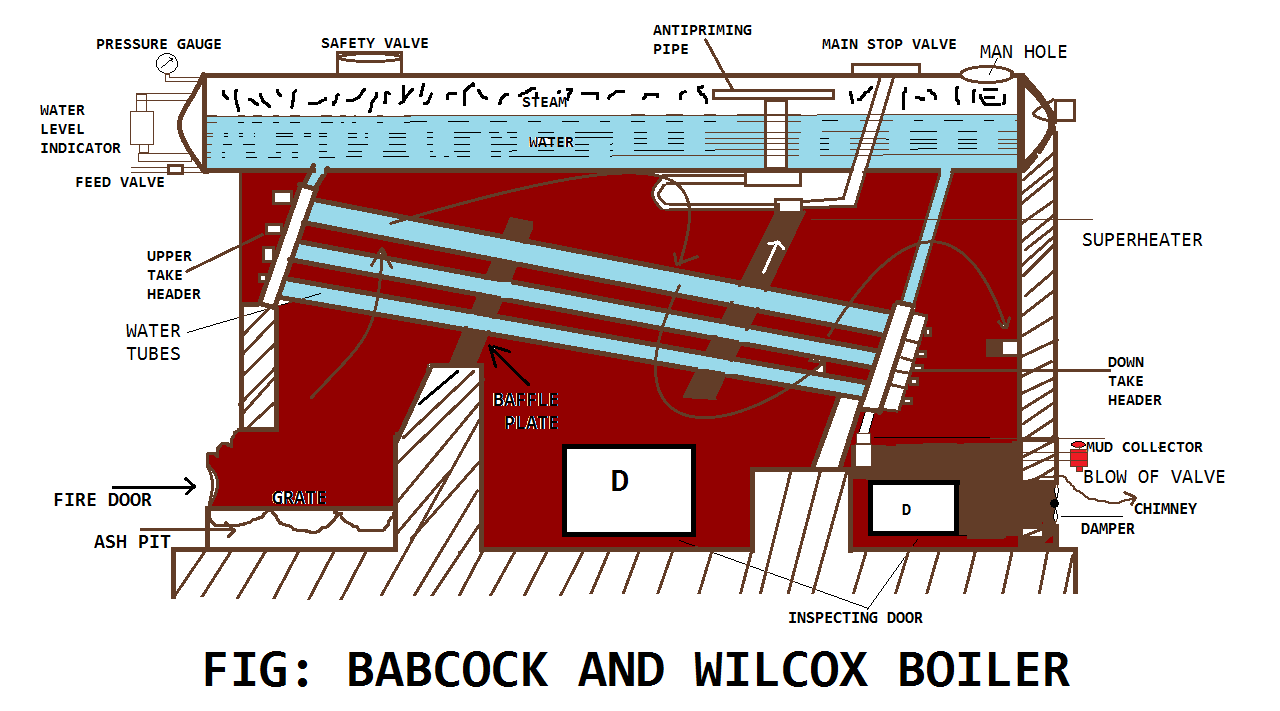

Babcock & Wilcox (BW) is a company built on the bones of the fossil fuel era. They know how to build big, heavy things that get very hot. The market wants to believe that this expertise translates perfectly into the "BrightLoop" hydrogen technology or their "SolveBright" carbon capture systems. It doesn't.

When you move from traditional coal and gas utility infrastructure to experimental chemical looping, you aren't just changing the fuel. You are changing the entire risk profile of the engineering. Most retail investors don't understand that "proven at pilot scale" is the graveyard of energy startups. Scaling a chemical process from a laboratory or a small test site to a utility-grade power plant involves exponential increases in mechanical stress, heat distribution failures, and catalyst degradation.

I have seen firms blow hundreds of millions trying to bridge the "valley of death" between a working prototype and a commercial asset. BW is trying to do this while carrying a legacy cost structure that would make a lean tech startup weep. They are fighting a two-front war: defending a shrinking core business in fossil fuels while trying to out-innovate venture-backed firms in the carbon capture space.

The Balance Sheet is the Real Story

Forget the "green" headlines for a moment. Look at the plumbing. A "great spec" usually implies a high-upside gamble. But a gamble only pays off if the house doesn't repossess your car while you're still at the table.

BW has spent years navigating a maze of restructuring, debt settlements, and preferred stock obligations. When a company’s interest expense starts eating a significant chunk of its operating income, they aren't innovating. They are treading water. They are forced to take "project wins" that might have razor-thin margins just to keep the cash flowing to satisfy creditors.

In the industrial sector, this leads to the "Bidding Curse." To show growth and keep the stock price alive, a struggling firm underbids on massive, complex construction contracts. If one thing goes wrong—a supply chain delay, a labor strike, or a miscalculation in steel prices—the project turns into a cash-shredder. I’ve watched this play out in the EPC (Engineering, Procurement, and Construction) world a dozen times. The "spec" isn't on the technology; it's a spec on whether they can manage a project without a catastrophic cost overrun.

Dismantling the Carbon Capture Fantasy

People asking "Is carbon capture the future?" are asking the wrong question. The right question is: "Who can actually get paid for it?"

The current hype cycle relies heavily on government subsidies like the 45Q tax credit in the United States. This creates an artificial market. If you are investing in BW because of their carbon capture tech, you are essentially betting on the permanence and efficiency of federal tax law. That is not a tech play. It's a political lobbying play.

Furthermore, the "SolveBright" system faces a commoditization problem. BW isn't the only player in the room. They are competing against global giants like Mitsubishi, Honeywell, and Schlumberger—companies with balance sheets that can absorb a billion-dollar mistake. BW doesn't have that luxury. In a "spec" scenario, the smaller player has to be significantly faster or better. There is zero evidence that BW's proprietary tech is so fundamentally superior that it overcomes the massive capital advantage of its competitors.

The Myth of the Pivot

The market loves a turnaround story. There’s a romantic notion that a 150-year-old company can "disrupt" itself. History suggests otherwise.

Institutional inertia is a physical force. When your entire middle management and engineering core is optimized for traditional boiler technology, transitioning to high-tech environmental solutions isn't just a matter of changing the marketing slides. It requires a complete cultural and operational overhaul.

Most companies in this position end up as "Zombie Industrials." They stay alive through a series of refinancings, asset sales, and occasional contract wins that provide just enough oxygen to prevent total collapse, but never enough fuel to actually launch. They are the walking dead of the Russell 2000.

The Hard Truth for the "Lightning Round" Crowd

If you want to gamble, go to Vegas. At least there, the drinks are free and the rules of the game are transparent.

Buying BW here means you believe they can:

- Successfully scale experimental hydrogen and carbon tech better than specialized startups.

- Out-compete multi-billion dollar conglomerates with 10x their R&D budget.

- Service a complex debt load while funding massive capital expenditures.

- Navigate the volatility of the energy transition without a single major project failure.

The probability of all four occurring simultaneously is statistically negligible.

How to Actually Play Clean Tech

Stop looking for the "legacy pivot." If you want exposure to the energy transition, look for the "arms dealers"—the companies providing the raw materials, the specialized sensors, or the software layers that are platform-agnostic.

Betting on a specific industrial firm to successfully transition its entire business model is the hardest way to make a buck in this market. You are taking on executive execution risk, technology risk, and macro-financial risk all at once.

The "Lightning Round" logic encourages you to look at a low share price and a familiar name and see "value." I look at the same data and see a trap designed for retail investors who think they've found a shortcut to the next Tesla. There are no shortcuts in heavy industry. There is only steel, heat, and the cold reality of the cash flow statement.

Stop listening to the noise. If a stock is described as a "great spec," it means the person saying it wouldn't put their own retirement fund in it. Neither should you.

Sell the hype. Watch the debt. Ignore the boilers.