The valuation of a startup is traditionally viewed through the lens of discounted cash flows or comparable exit multiples, yet the most significant lever for net realized wealth often resides in the tax treatment of the exit itself rather than the nominal sale price. The proposed modifications to capital gains structures within the 2026 legislative framework do not merely adjust a percentage; they re-engineer the risk-reward calculus for founders and early-stage employees by expanding the eligibility and efficacy of Section 1202, commonly known as Qualified Small Business Stock (QSBS).

The Mechanics of Enhanced Section 1202 Eligibility

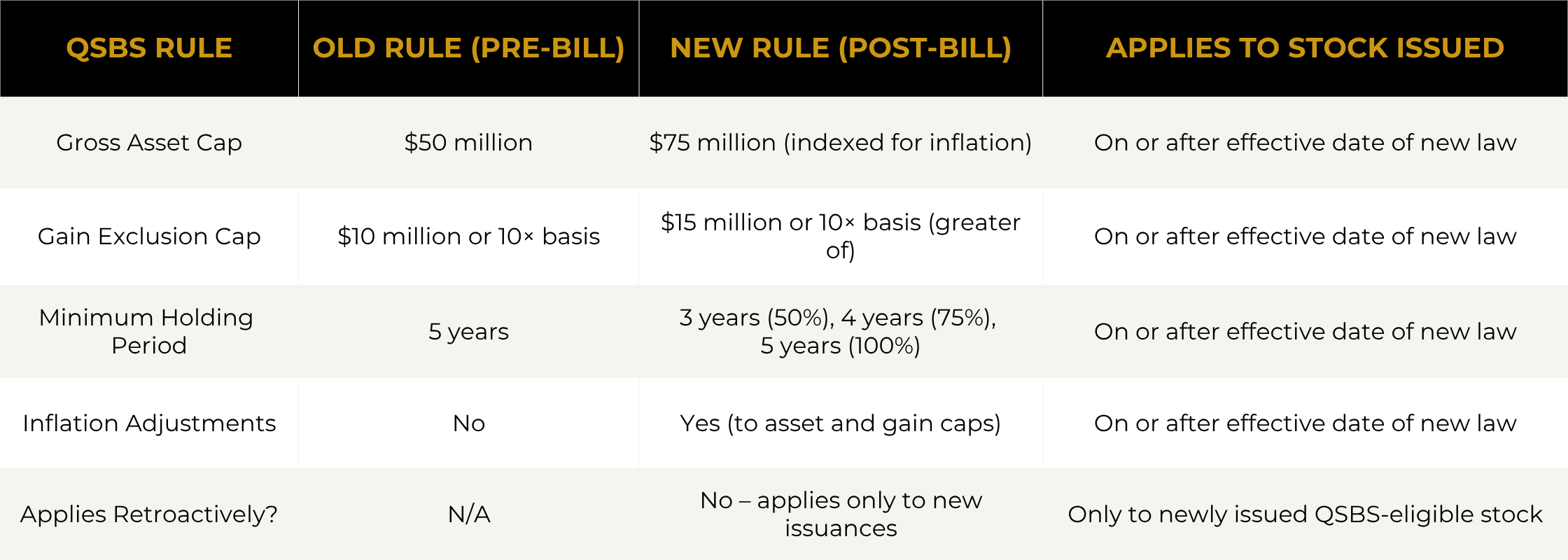

Section 1202 currently allows non-corporate taxpayers to exclude up to 100% of the gain from the sale of qualified small business stock held for more than five years, subject to a cap of the greater of $10 million or 10 times the taxpayer’s basis. The legislative shift focuses on three structural friction points that previously limited the utility of this "boon" for the broader tech and manufacturing sectors.

1. The Gross Asset Test Threshold

The current $50 million gross asset limit acts as a growth ceiling. Under the new proposal, this threshold faces upward revision to account for inflationary pressures and the increased capital intensity required for modern hardware and AI infrastructure. By raising the ceiling, a wider cohort of "Scale-ups"—companies that have moved beyond the seed stage but remain in high-growth phases—can continue to issue QSBS-eligible shares to new hires.

2. The 80% Active Business Requirement

For a corporation's stock to qualify, at least 80% of its assets must be used in the active conduct of one or more qualified trades or businesses. The new bill seeks to clarify the treatment of intellectual property and R&D credits within this 80% calculation. For founders, this reduces the "audit anxiety" associated with holding significant cash reserves from a recent funding round, which previously threatened to tip the asset balance toward "investment" rather than "active" use.

3. The Modification of the Holding Period Bridge

The five-year holding period remains the primary hurdle for liquidity. The strategy being introduced involves a "tacking" mechanism or a shortened bridge for businesses in specific strategic sectors (semiconductors, domestic energy, and aerospace). This effectively compresses the time-to-value for early employees, making equity compensation mathematically superior to higher base salaries even in a high-interest-rate environment.

The Capital Concentration Effect

When the effective tax rate on a specific asset class drops to 0%, the internal rate of return (IRR) for those assets is structurally disconnected from the broader market's capital gains rate. This creates a "Concentration Effect" where founders and early employees are incentivized to maintain high-equity, low-cash compensation structures for longer durations.

A $1,000,000 gain on traditional capital gains at a projected 28.8% rate (inclusive of the Net Investment Income Tax) yields $712,000 post-tax. The same gain under 100% QSBS exclusion yields $1,000,000. For an early employee with 0.1% of a $1B exit, the difference is a $288,000 "tax tax" that the new bill effectively subsidizes.

The Three Pillars of Founders’ Exit Optimization

- The Basis Expansion Pillar: The 10x basis rule under Section 1202 allows founders who contribute significant initial capital or assets to the corporation at formation to potentially exclude significantly more than the $10 million cap. The new legislation facilitates easier rollovers and basis adjustments that benefit early-stage investors over late-stage institutional capital.

- The Stacking Pillar: By gifting shares to family members or non-grantor trusts, founders can "stack" the $10 million exclusion across multiple taxpayers. The 2026 bill addresses the "related party" rules that previously hampered this strategy, making it a viable wealth-transfer mechanism before a liquidity event.

- The Diversification Pillar (Section 1045): Section 1045 allows for the rollover of QSBS gains into another QSB without immediate tax recognition. The new policy environment simplifies the rollover process, encouraging "serial entrepreneurship" by allowing founders to recycle capital into new ventures with zero friction from the tax authorities.

Addressing the High-Growth Equity Paradox

The primary limitation of the current and proposed QSBS expansion is the "qualified trade or business" definition. Section 1202(e)(3) specifically excludes certain service businesses, including law, engineering, and financial services. The 2026 bill’s impact on "business founders" is therefore asymmetrical; it heavily favors product-based companies over service-based agencies.

For the "early employee" cohort, this creates a bifurcated labor market. Talent will gravitate toward companies where the equity package carries the QSBS-eligible "stamp of approval." This acts as a secondary filter for top-tier engineers and product managers, who now increasingly demand a "Tax Opinion" or at least a "QSBS Eligibility Analysis" as part of their employment offer package.

Operational Risks for Early-Stage Hires

- The Redemption Risk: If a company redeems more than 5% of its stock within a specific two-year period, it can disqualify all stock issued during that time from being QSBS-eligible.

- The S-Corp Trap: Many startups begin as S-Corporations for tax flexibility but must convert to C-Corporations to issue QSBS. The timing of this conversion is critical; only stock issued after the conversion is eligible.

- The Asset Ceiling Breach: If a company raises a massive Series B that pushes its gross assets above $50M (or the new proposed ceiling), all shares issued prior to that event remain eligible, but all shares issued afterward are standard capital gains assets.

Strategic Capital Deployment and Tactical Response

The 2026 bill’s expansion of capital gains benefits for founders and employees is not a passive windfall; it is a structural incentive to build and hold high-growth, high-asset companies. The shift from 15% or 20% capital gains toward a 0% effective rate for qualified startups represents a massive reallocation of potential tax revenue toward private wealth creation.

For founders, the strategy is twofold: ensure C-Corp status from day zero and aggressively manage the gross asset test through lean operations or debt-heavy financing that does not count toward the $50M equity asset limit. For early employees, the play is to demand clarity on the issuance date and the company's "qualified" status during every annual review.

The true value of this tax change is not the "boon" to existing wealth, but the lowering of the barrier for the next generation of industrial and technological founders who can now compete with the liquidity of the public markets through the sheer magnitude of their post-tax exit potential.

Would you like me to analyze the specific sectors that qualify as "strategic" under the 2026 bill to see how they differ from the traditional Section 1202 exclusions?